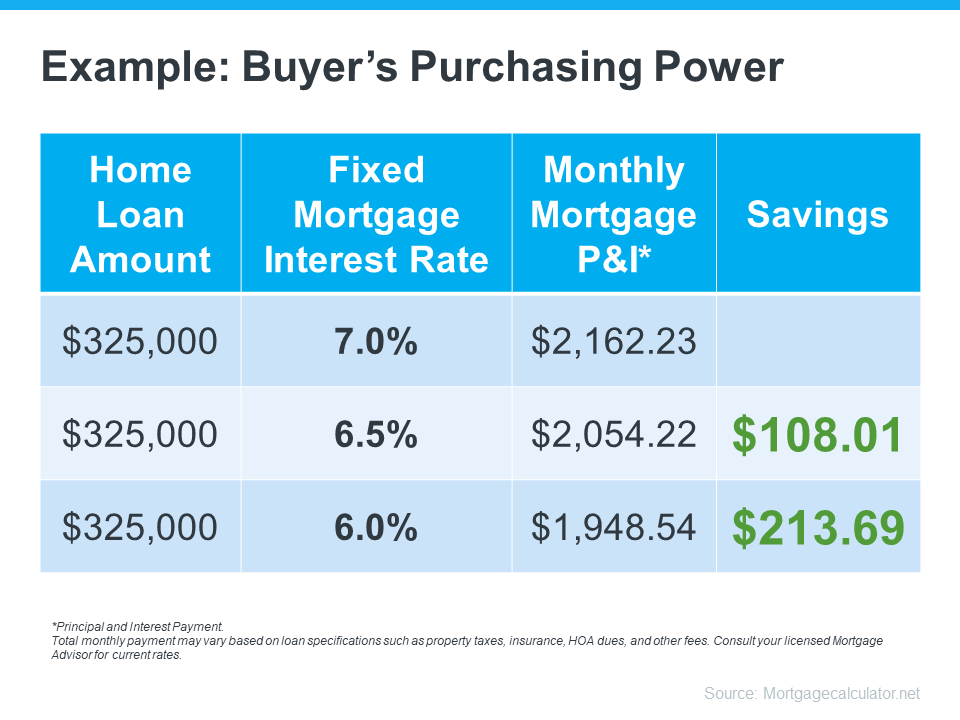

When it comes to buying a home, especially with today’s affordability challenges, you’ll want to be strategic. Mortgage rates impact how much it costs to borrow money for your home loan. And, to help offset the higher borrowing costs today, some homebuyers are taking a close look at their wish list and re-evaluating what features they really need in their next home to avoid overextending. As a recent NerdWallet article says:

“A pool, for example, may be nice to have, but it may not provide as much day-to-day value as a garage or a space for a home office . . .”

While that pool may be appealing, think twice about whether or not it’s really something you must have to be happy in your next home. Is getting that pool the main reason you’re moving? Probably not. It’s more likely a need for more space, a home office, or proximity to loved ones, friends, or work that’s motivating you to make a change.

Evaluating Your Wants and Needs as a Homebuyer

So, if you’re looking to buy a home, take some time to consider what’s truly essential for you in your next house. Make a list of all the features you’ll want to see, and from there, work to break those features into categories. Here’s a great way to organize your list:

want to see, and from there, work to break those features into categories. Here’s a great way to organize your list:

- Must-Haves – If a house doesn’t have these features, it won’t work for you and your lifestyle (examples: distance from work or loved ones, number of bedrooms/bathrooms, etc.).

- Nice-To-Haves – These are features you’d love to have but can live without. Nice-to-haves aren’t dealbreakers, but if you find a home that hits all the must-haves and some of these, it’s a contender (examples: a second home office, a garage, etc.).

- Dream State – This is where you can really think big. Again, these aren’t features you’ll need, but if you find a home in your budget that has all the must-haves, most of the nice-to-haves, and any of these, it’s a clear winner (examples: a pool, multiple walk-in closets, etc.).

Once you’ve categorized it in a way that works for you, discuss your top priorities with your real estate agent. Remember to think carefully about what’s a non-negotiable for your lifestyle and what’s a nice-to-have that’s more of an added bonus. Be sure to discuss where each feature falls with your agent. They’ll be able to help you refine the list further, coach you through the best way to stick to it, and find a home in your area that meets your top needs.

Bottom Line

Bottom Line

Putting together your list of necessary features for your next home might seem like a small task, but it’s a crucial planning step on your home-buying journey today. For a no-obligation mortgage consultation or a mortgage pre-approval, contact Jim Riley today at 612-968-2601 or email jriley@unitedfamilymortgage.com.

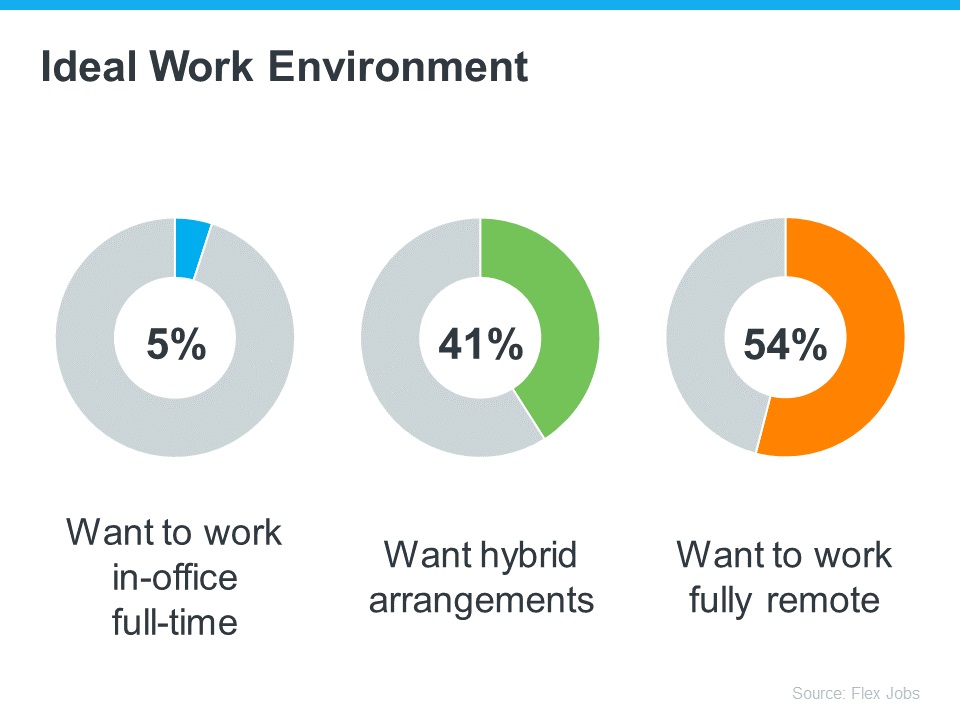

Remote or hybrid work opens up a world of opportunities. That’s because it allows you to broaden your search for your next home since you’re no longer limited to living close to your workplace. With the freedom to work from anywhere, you can explore more affordable areas that may be located farther away from bustling city centers or your office. This flexibility can be a game changer while higher mortgage rates are making it difficult for some homebuyers to afford a home.

Remote or hybrid work opens up a world of opportunities. That’s because it allows you to broaden your search for your next home since you’re no longer limited to living close to your workplace. With the freedom to work from anywhere, you can explore more affordable areas that may be located farther away from bustling city centers or your office. This flexibility can be a game changer while higher mortgage rates are making it difficult for some homebuyers to afford a home.

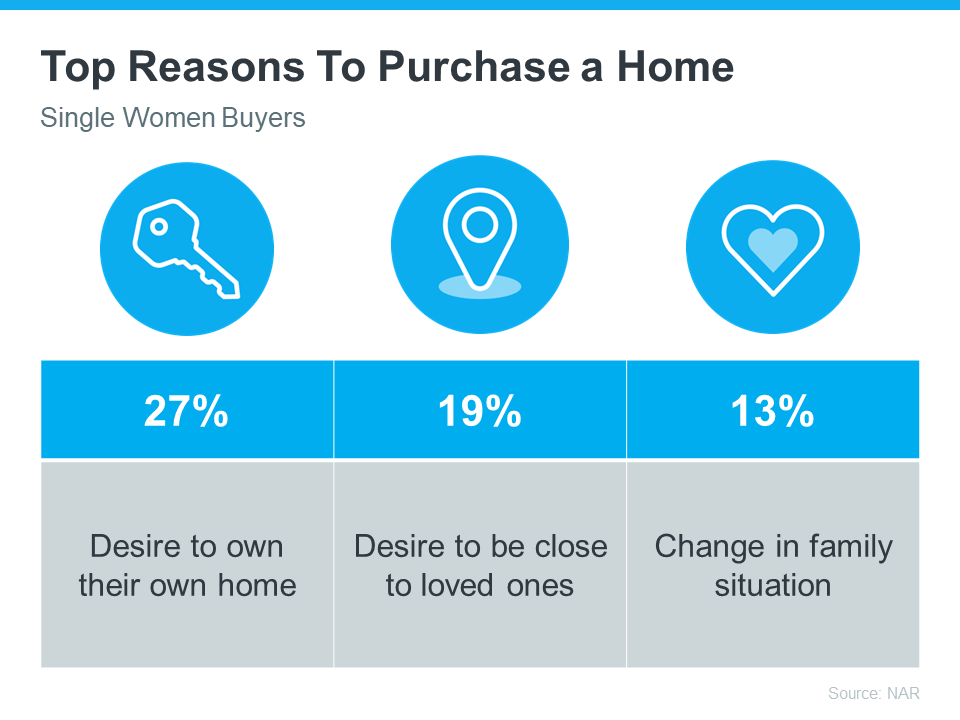

Why Is Homeownership So Important to Women?

Why Is Homeownership So Important to Women?

What This Means for You

What This Means for You