Throughout Women’s History Month, we reflect on the impact women have in our lives, and that includes the impact on the housing market. In fact, since at least 1981, single women have bought more homes than single men each year, and they make up 17% of all households.

Why Is Homeownership So Important to Women?

Why Is Homeownership So Important to Women?

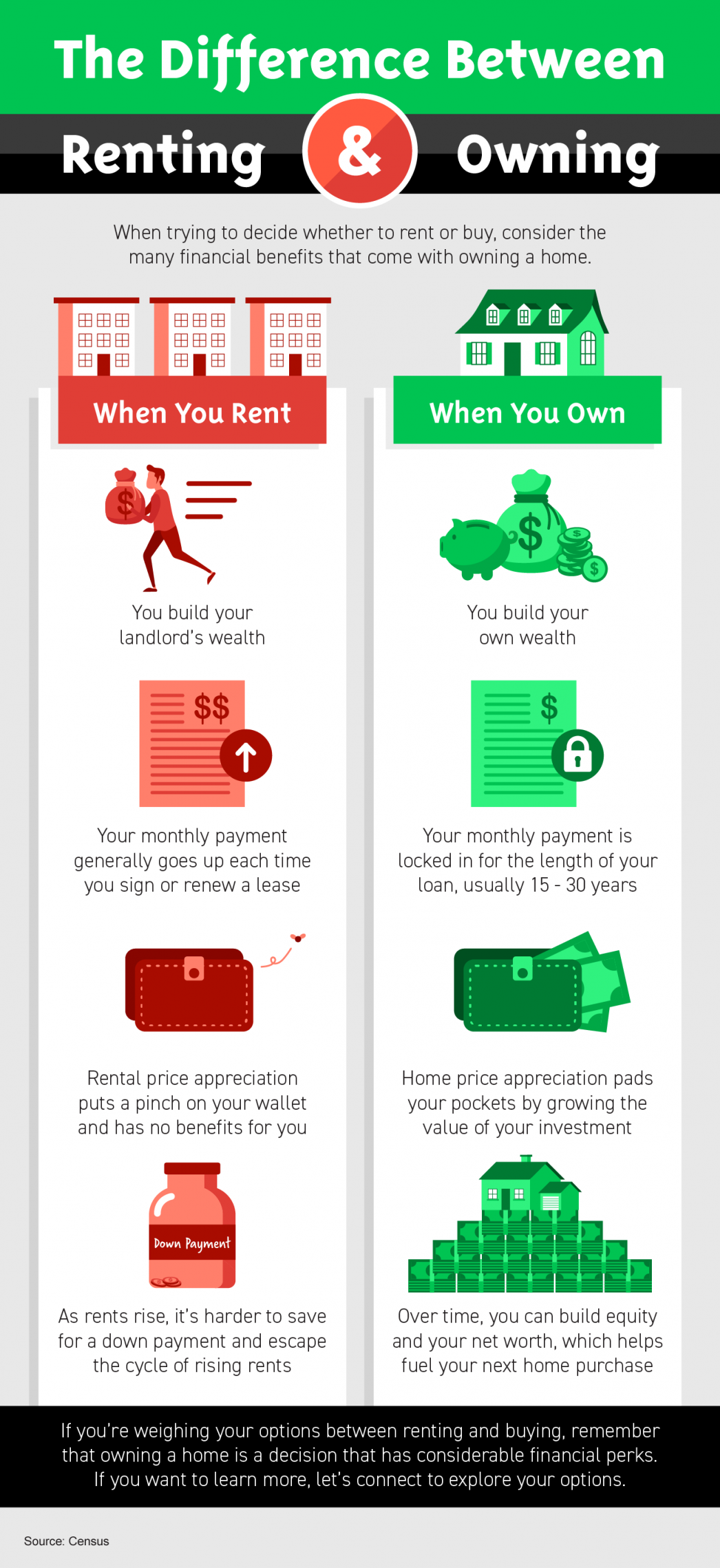

The rise in women pursuing homeownership hasn’t just made an impact on the housing market. It’s also been an asset for those buyers and their households. That’s because homeownership has many benefits, both financial and personal.

On the financial side, housing proves to be the key to building wealth for single women. Ksenia Potapov, Economist at First American, says:

“For single women, housing has always made up a large share of total assets. Over the last 30 years, the average single woman’s wealth has increased 88% on an inflation-adjusted basis, from just over $142,000 in 1989 to $267,000 in 2019, and housing has remained the single largest component of their wealth.”

The financial security and independence homeownership provides can be life-changing, too. And when you factor in the personal motivations behind buying a home, that impact becomes even clearer.

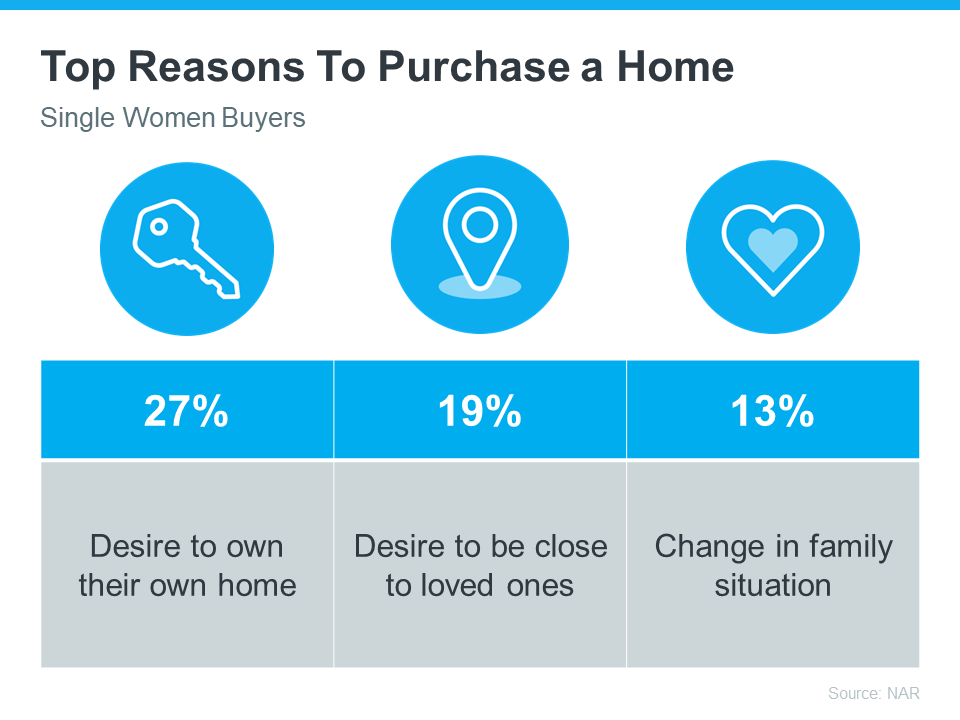

A recent report from the National Association of Realtors (NAR) shares the top reasons single women are buying a home right now (see chart below):

Bottom Line

Homeownership can be life-changing no matter who you are. At United Family Mortgage, we get it! United Family Mortgage is a Mortgage Broker. We shop for mortgage deals for our borrowers, from conventional low-interest mortgages and low-down-payment mortgages to zero-downpayment options and VA (veteran) mortgages.

So why get a personal shopper, like United Family Mortgage, for your mortgage? Because you want an advocate, not an order taker. For a no-obligation mortgage consultation or a mortgage pre-approval, contact us today at 763-241-0306.

For a hassle-free mortgage consultation or a second opinion, contact Jennifer Baldwin with United Family Mortgage today at 612-743-5077 or email

For a hassle-free mortgage consultation or a second opinion, contact Jennifer Baldwin with United Family Mortgage today at 612-743-5077 or email