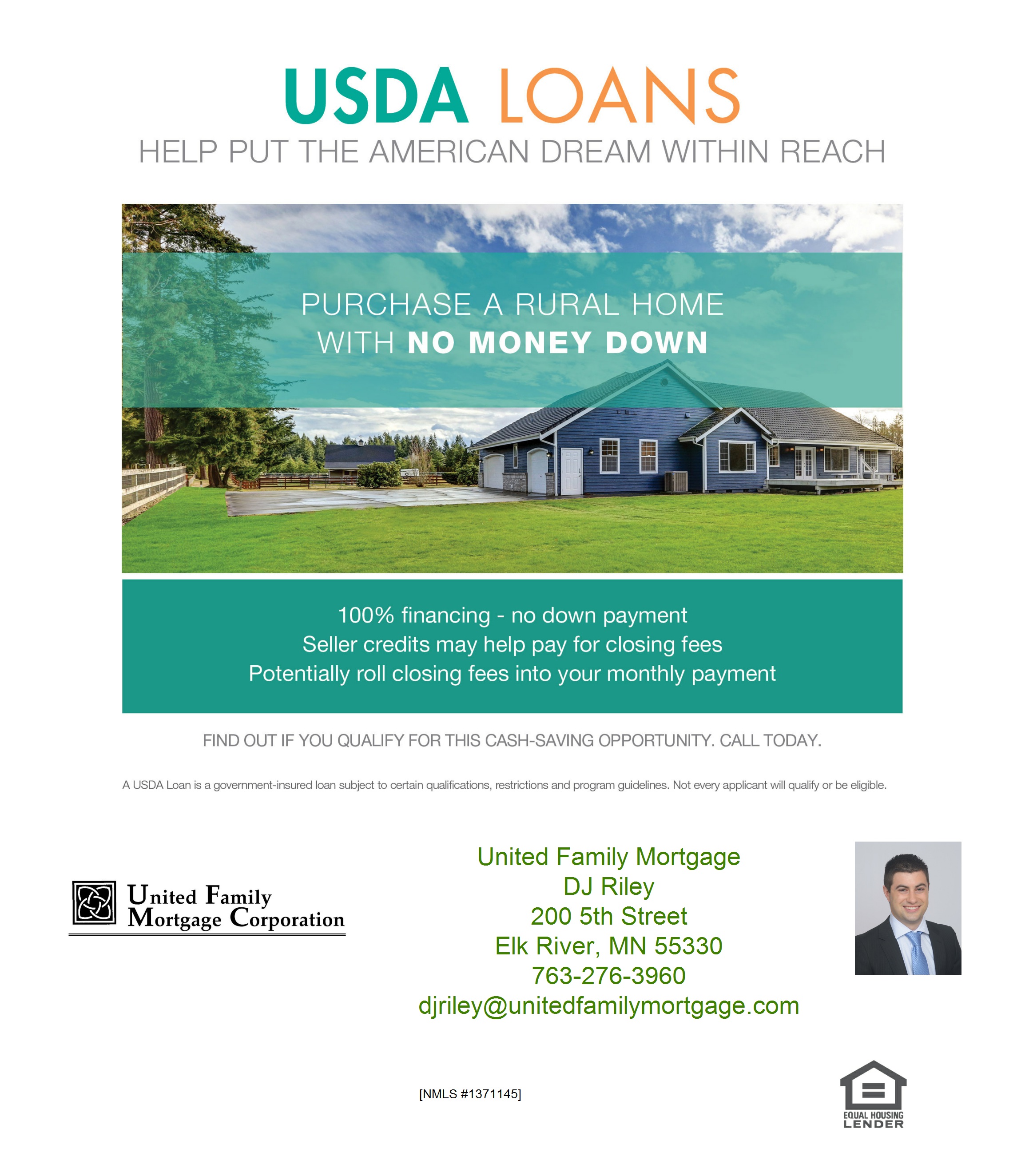

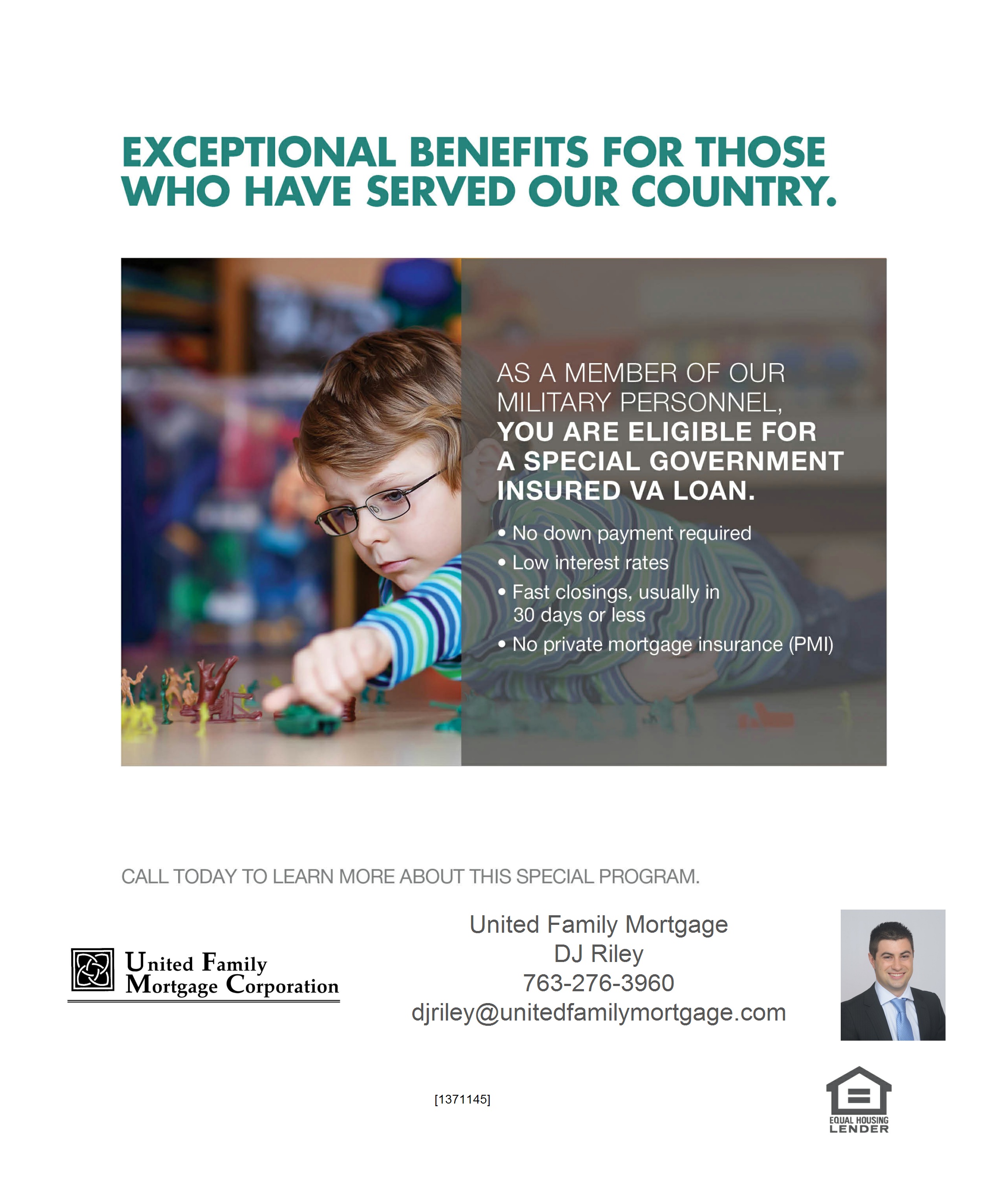

To schedule a hassle-free phone consultation, contact DJ Riley, click here.

Elk River: 763-241-0306 | Monticello: 763-276-3960 | Fax: 763-241-0323

NMLS# - 323175

The largest obstacle renters face when planning to buy a home is saving for a down payment. This challenge is amplified by rising rents, which has eaten into the amount of money renters have leftover for savings each month after paying expenses.

In combination with higher rents, survey after survey has shown that non-homeowners (renters and those living rent-free with family or friends) believe they need to save upwards of 20% for their down payment!

According to the “Barriers to Accessing Homeownership” study commissioned in partnership between the Urban Institute, Down Payment Resource, and Freddie Mac, 39% of non-homeowners and 30% of those who already own a home believe they need more than a 20% down payment.

The percentage of those who are aware of low down payment programs (those under 5%) is surprisingly low at 12% for non-homeowners and 13% for homeowners.

In a recent Convergys Analytics report, they found that 49% of renters believe they need at least a 20% down payment.

The median down payment on loans approved in 2018 was only 5%! Those waiting until they have over 20% may already have enough saved to buy now!

There are over 45 million millennials (33%) who are mortgage ready right now, meaning their income, debt, and credit scores would all allow them to qualify for a mortgage today!

If your five-year plan includes buying a home, let’s get together to determine what it will take to make that plan a reality. You may be closer to your dream than you realize!

For a hassle-free first-time home buyer mortgage consultation, contact DJ Riley today at 763-276-3960 or via email @ djriley@unitedfamilymortgage.com.

0 Down Mortgage Ramsey, MN | Apply for VA Home Loan Elk River | Apply for VA Home Loan Monticello | Apply for VA Home Loan Ramsey, MN | Apply for VA Home Loan Zimmerman | Best Mortgage Rates Today Ramsey, MN | Down Payment Assistance Elk River | Down Payment Assistance Ramsey, MN | Down Payment Assistance Zimmerman | FHA Approved Lenders Ramsey, MN | FHA Mortgage Interest Rates Ramsey, MN | Home Construction Loans Ramsey, MN | Home Loans with No Down Payment Ramsey, MN | Mortgage Broker Otsego | Mortgage Broker Ramsey, MN | Mortgage Broker Rogers | Mortgage Broker Zimmerman | Veteran Home Loan Ramsey, MN | VA Home Loan Ramsey, MN | VA Home Loan Monticello

There are some people who haven’t purchased homes because they are uncomfortable taking on the obligation of a mortgage. However, everyone should realize that unless you are living with your parents rent-free, you are paying a mortgage – either yours or your landlord’s.

As Entrepreneur Magazine, a premier source for small business explained in their article, “12 Practical Steps to Getting Rich”:

“While renting on a temporary basis isn’t terrible, you should most certainly own the roof over your head if you’re serious about your finances. It won’t make you rich overnight, but by renting, you’re paying someone else’s mortgage. In effect, you’re making someone else rich.”

With home prices rising, many renters are concerned about their house-buying power. Mike Fratantoni, Chief Economist at MBA, explained:

“The spring homebuying season is almost upon us, and if rates stay lower, inventory continues to grow, and the job market maintains its strength, we do expect to see a solid spring market.”

As an owner, your mortgage payment is a form of ‘forced savings,’ which allows you to build equity in your home that you can tap into later in life. As a renter, you guarantee the landlord is the person building that equity.

As mentioned before, interest rates are still at historic lows, making it one of the best times to secure a mortgage and make a move into your dream home. Freddie Mac’s latest report shows that rates across the country were at 4.46% last week.

Whether you are looking for a primary residence for the first time or are considering a vacation home on the shore, now may be the time to buy.

For a hassle-free first-time home buyer mortgage consultation, contact DJ Riley today at 763-276-3960 or via email @ djriley@unitedfamilymortgage.com.

0 Down Mortgage Ramsey, MN | Apply for VA Home Loan Elk River | Apply for VA Home Loan Monticello | Apply for VA Home Loan Ramsey, MN | Apply for VA Home Loan Zimmerman | Best Mortgage Rates Today Ramsey, MN | Down Payment Assistance Elk River | Down Payment Assistance Ramsey, MN | Down Payment Assistance Zimmerman | FHA Approved Lenders Ramsey, MN | FHA Mortgage Interest Rates Ramsey, MN | Home Construction Loans Ramsey, MN | Home Loans with No Down Payment Ramsey, MN | Mortgage Broker Otsego | Mortgage Broker Ramsey, MN | Mortgage Broker Rogers | Mortgage Broker Zimmerman | Veteran Home Loan Ramsey, MN | VA Home Loan Ramsey, MN | VA Home Loan Monticello

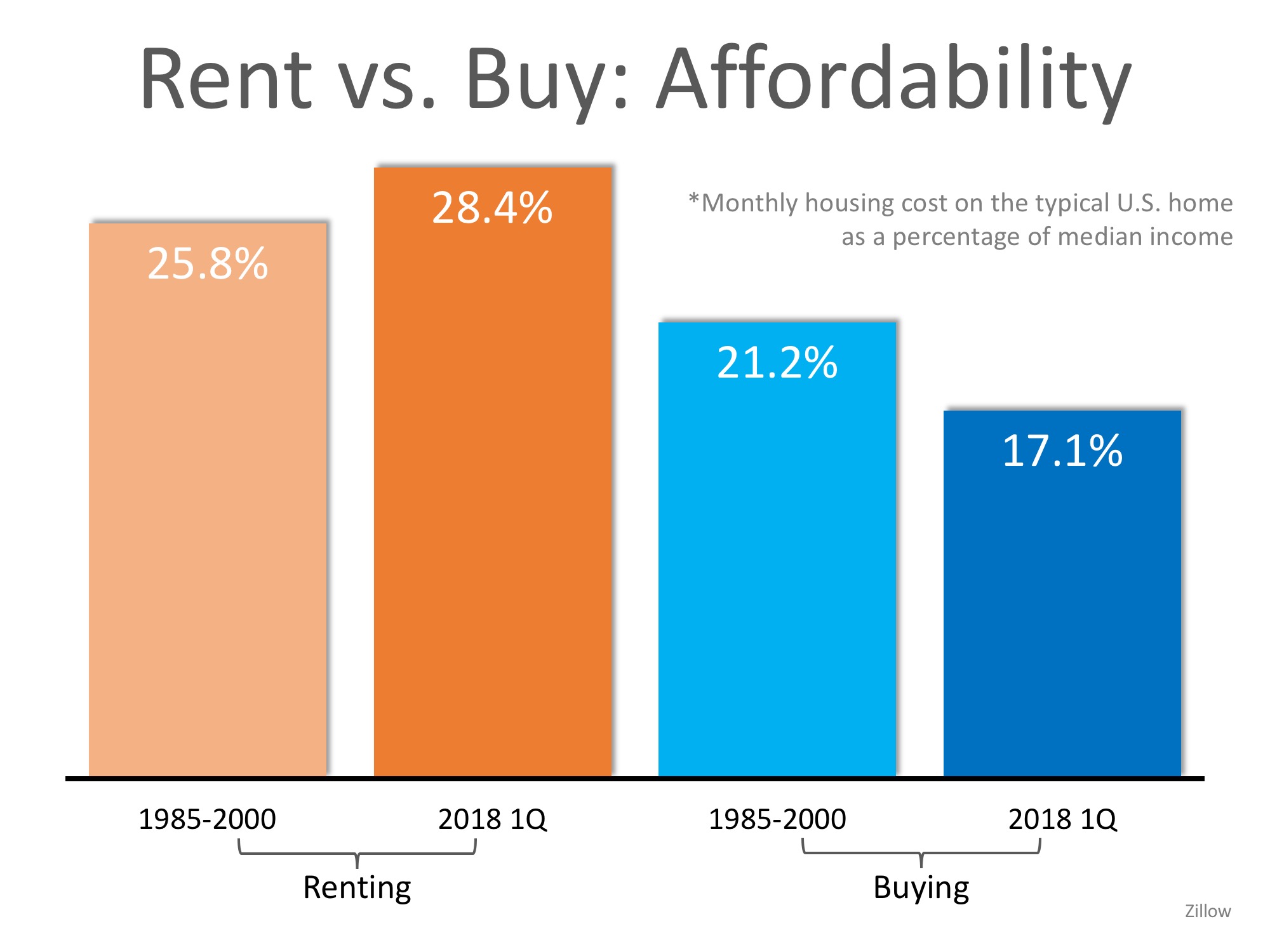

Chances are if you are renting you are spending too much of your income on your monthly housing expense. There is a long-standing ‘rule’ that a household should not pay more than 28% of their income on their rent or mortgage payment. This percentage allows the household to save money for the future while comfortably covering other expenses.

According to new data released from ApartmentList.com, 49.5 million renters in the United States were cost-burdened in 2017, meaning they spent more than 30% of their monthly incomes on rent. This accounts for nearly half of all renter households in the country and is up 3.1 million from 2007.

When a household is cost-burdened by their monthly housing expense, they are not as easily able to save money for the future. This is a big factor for many renters who dream of owning their own homes someday.

But there is hope for those who are able to save at least a 3% down payment! The percentage of income needed in the US to buy a home is significantly less than renting at 17.1%!

The chart below compares the historic percentage of income needed to rent and buy from 1985-2000 to the first quarter of 2018. As you can see, the cost of renting has climbed above historic numbers while the cost of buying dropped over the same period of time.

If you are one of the many renters who is spending too much of their monthly income on rent, consider saving money by getting a roommate, moving into a less expensive apartment, or even moving in with family. These are all ways to save for a down payment so that you can put your housing costs to work for you!

To schedule a hassle-free mortgage consultation, contact DJ Riley today at 763-276-3960, or via email @djriley@unitedfamilymortgage.com.

The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

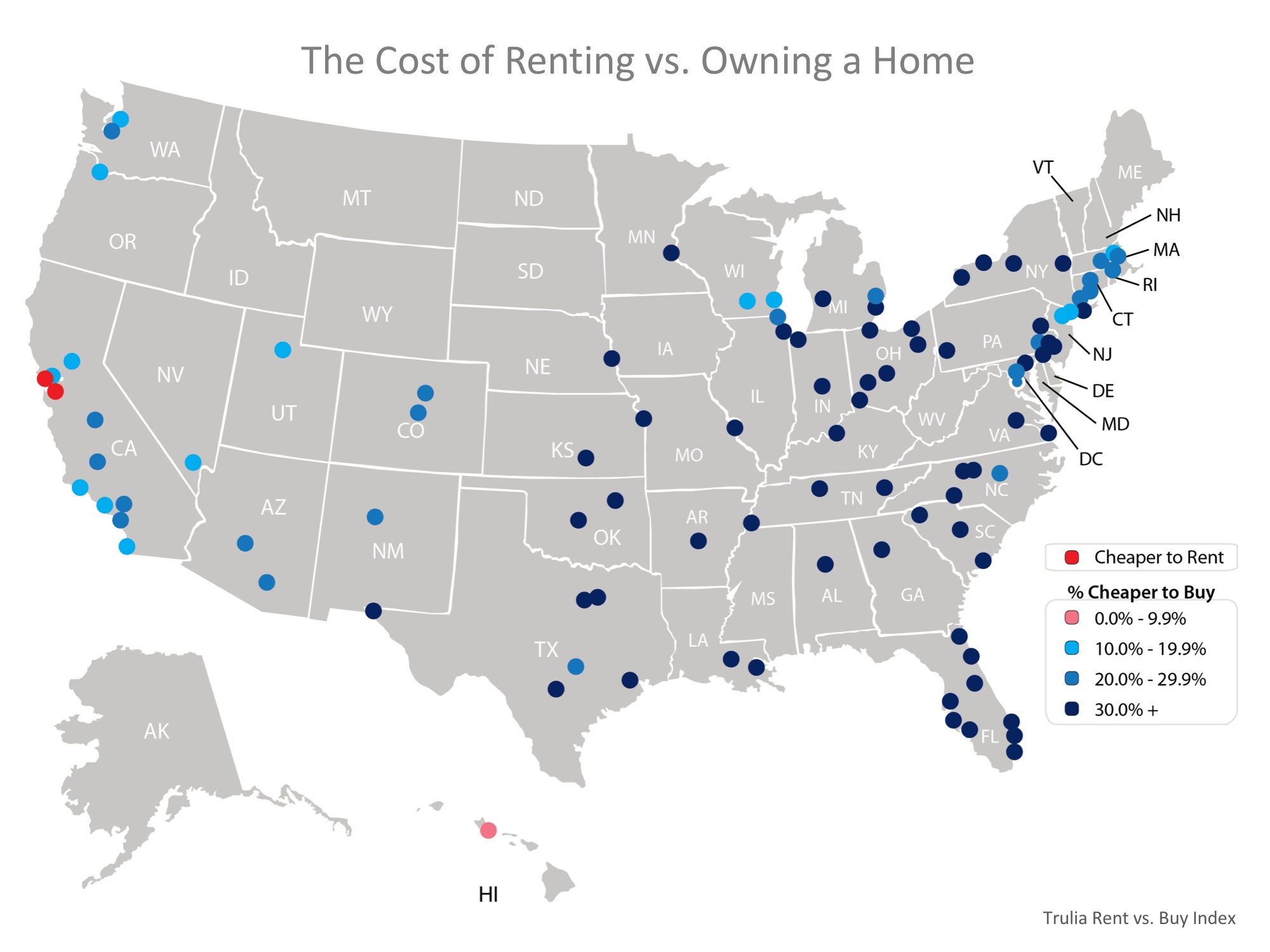

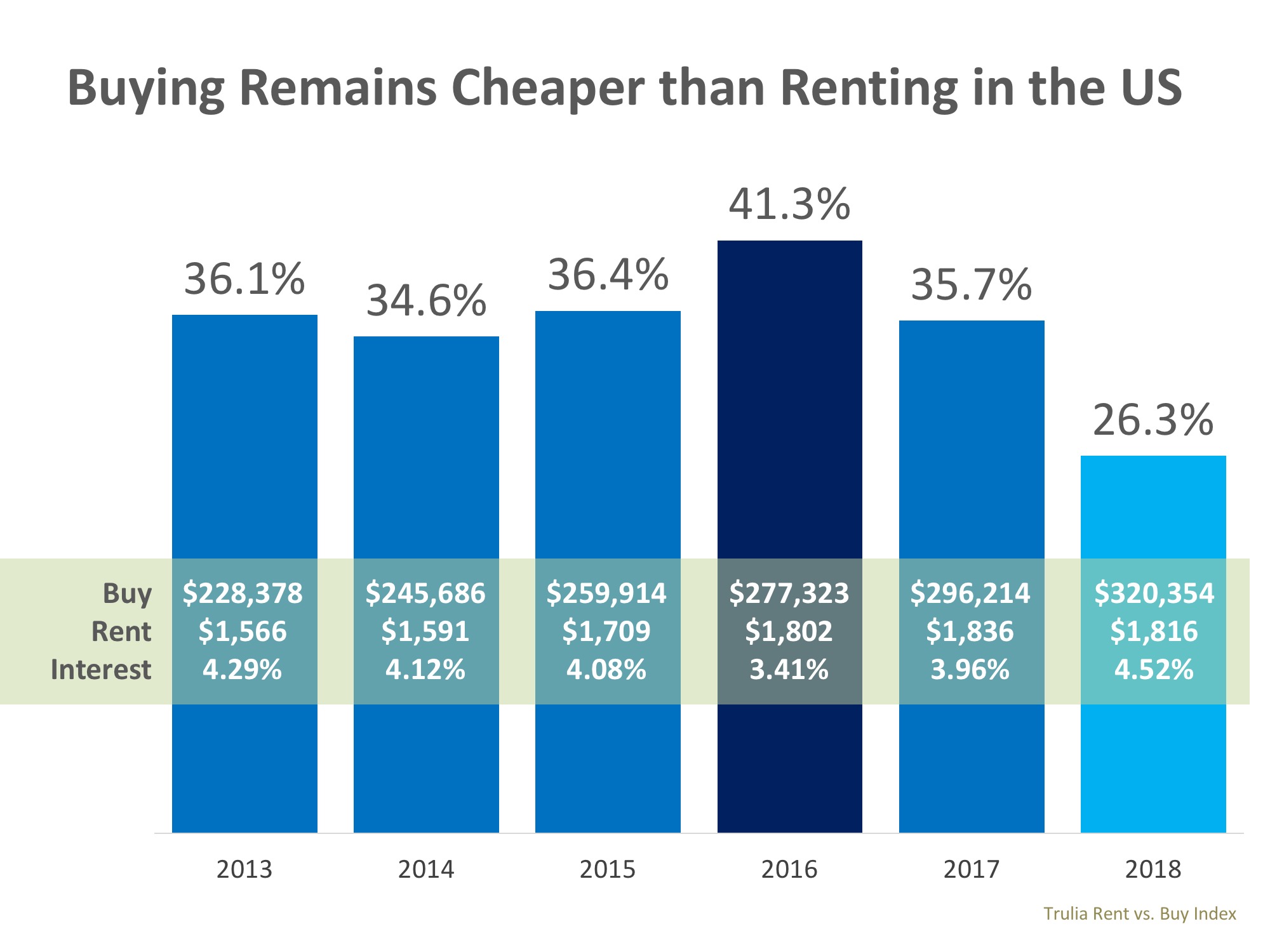

The results of the latest Rent vs. Buy Report from Trulia show that homeownership remains cheaper than renting, with a traditional 30-year fixed rate mortgage, in 98 of the 100 largest metro areas in the United States.

In the six years that Trulia has conducted this study, this is the first time that it was cheaper to rent than buy in any of the metropolitan areas.

It’s no surprise, however, that those two metros are San Jose and San Francisco, CA, where median home prices have jumped to over $1 million dollars this year. Home values in San Jose have risen 29% in the last year, while rents have remained relatively unchanged.

For the 98 metros where homeownership wins out, 97 of them show a double-digit advantage when buying. The range is an average of 2.0% less expensive in Honolulu (HI), all the way up to 48.9% in Detroit (MI), and 26.3% nationwide!

Below is a map of the 100 metros that were studied. The darker the blue dot on the metro, the cheaper it is to buy there.

In order to calculate the true cost of renting vs. buying, Trulia includes all assumed renting costs, including one-time costs (like security deposits), and compares them to the monthly costs of owning a home (insurance, mortgage payments, taxes, and maintenance) including one-time costs (down payments, closing costs, sale proceeds). They also assume that households stay in their home for seven years, put down a 20% down payment, and take out a 30-year fixed rate mortgage. The full methodology is included with the study results here.

Below is a chart created with the data from the last six years of the study, showing the impact of the median home price, rental price, and 30-year fixed rate interest rate used to calculate the ‘cheaper to buy’ metric.

In 2016, when buying was 41.3% less expensive than renting, the average mortgage rate was the driving force behind the difference. Rates this year are the highest they have been in six years which has narrowed the gap, all while home price appreciation has also been driven up by a lack of homes for sale.

Cheryl Young, Trulia’s Chief Economist, had this to say,

“One point deserves emphasizing: The ultra-costly San Francisco Bay Area is not a harbinger for the nation as a whole. While renting may outweigh buying in San Jose and San Francisco, it is unlikely that renting will tip the scales nationally anytime soon.”

Homeownership provides many benefits beyond the financial ones. If you are one of the many renters out there who would like to evaluate your ability to buy this year, let’s get together to find your dream home.

To schedule a hassle-free mortgage consultation, contact DJ Riley today at 763-276-3960, or via email @ djriley@unitedfamilymortgage.com.

The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

We have all seen the headlines that report that buying a home is less affordable today than it was at any other time in the last ten years, and those headlines are accurate. But, have you ever wondered why the headlines don’t say the last 25 years, the last 20 years, or even the last 11 years?

Obviously, buying a home is more expensive now than during the ten years immediately following one of the worst housing crashes in American history.

Over the past decade, the market was flooded with distressed properties (foreclosures and short sales) that were selling at 10-50% discounts. There were so many distressed properties that the prices of non-distressed properties in the same neighborhoods were lowered and mortgage rates were kept low to help the economy.

Prices have since recovered and mortgage rates have increased as the economy has gained strength. This has and will continue to impact housing affordability moving forward.

However, let’s give affordability some historical context. The National Association of Realtors (NAR) issues their Affordability Index each month. According to NAR:

“The Monthly Housing Affordability Index measures whether or not a typical family earns enough income to qualify for a mortgage loan on a typical home at the national and regional levels based on the most recent monthly price and income data.”

NAR’s current index stands at 138.8. The index had been higher each of the last ten years, peaking at 197 in 2012 (the higher the index the more affordable houses are).

But, the average index between 1990 and 2007 was just 123 and there were no years with an index above 133. That means that homes are more affordable today than at any time during the eighteen years between 1990 and 2007.

With home prices continuing to appreciate and mortgage rates increasing, home affordability will likely continue to slide. However, this does not mean that buying a house is not an attainable goal in most markets as it is less expensive today than during the eighteen-year stretch immediately preceding the housing bubble and crash.

To schedule a hassle-free mortgage consultation, contact DJ Riley today at 763-276-3960, or via email @ djriley@unitedfamilymortgage.com. Mortgage Broker Monticello | Mortgage Broker Ramsey | Mortgage Broker Elk River | Mortgage Broker Otsego | Mortgage Broker Rogers | Mortgage Broker Big Lake | Mortgage Broker Zimmerman | Mortgage Broker Albertville | Mortgage Broker St. Michael

The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

Recently, multiple headlines have been written asserting that homeownership is less affordable today than at any other time in the last decade. Though the headlines are accurate, they lack context and lead too many Americans to believe that they can’t partake in a major part of the American Dream – owning a home.

In 2008, the housing market crashed and home values fell by as much as 60% in certain markets. This was the major trigger to the Great Recession we experienced from 2008 to 2010. To come back from that recession, mortgage interest rates were pushed down to levels that were never seen before.

For the last ten years, you could purchase a home at a dramatically discounted price and attain a mortgage at a historically low mortgage rate.

Affordability skyrocketed.

Now that home values have returned to where they should be, and mortgage rates are beginning to increase, it is less affordable to own a home than it was over the last ten years.

However, what is not being reported is that it is MORE AFFORDABLE to own a home today than at any other time since 1985 (when data was first collected on this point).

If you take out the years after the crash, affordability today is greater than it has been at almost any time in American history.

This has not been adequately reported which has led to many Americans believing that they cannot currently afford a home.

As an example, the latest edition of Freddie Mac’s Research: Profile of Today’s Renter reveals that 75% of renters now believe it is more affordable to rent than to own their own homes. This percentage is the highest ever recorded. The challenge is that this belief is incorrect. Study after study has proven that in today’s market, it is less expensive to own a home than it is to rent a home in the United States.

Thankfully, some are starting to see this situation and accurately report on it. The National Association of Realtors, in their 2019 Housing Forecast, mentions this concern:

“While the U.S. is experiencing historically normal levels of affordability, potential buyers may be staying out of the market because of perceived problems with affordability.”

If you are one of the many renters who would like to own their own homes, let’s get together to find out if homeownership is affordable for you right now.

To schedule a hassle-free mortgage consultation, contact DJ Riley today at 763-276-3960, or via email @ djriley@unitedfamilymortgage.com. Mortgage Broker Monticello | Mortgage Broker Ramsey | Mortgage Broker Elk River | Mortgage Broker Otsego | Mortgage Broker Rogers | Mortgage Broker Big Lake | Mortgage Broker Zimmerman | Mortgage Broker Albertville | Mortgage Broker St. Michael

The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.