Since the creation of the Veterans Affairs (VA) Home Loans Program, over 22 million veterans have achieved the American Dream of homeownership. Many veterans do not know the details of the program and therefore do not take advantage of the benefits available to them.

If you are a veteran or you know someone who is, here is a breakdown of the VA Home Loan benefits that can be used to achieve the American Dream!

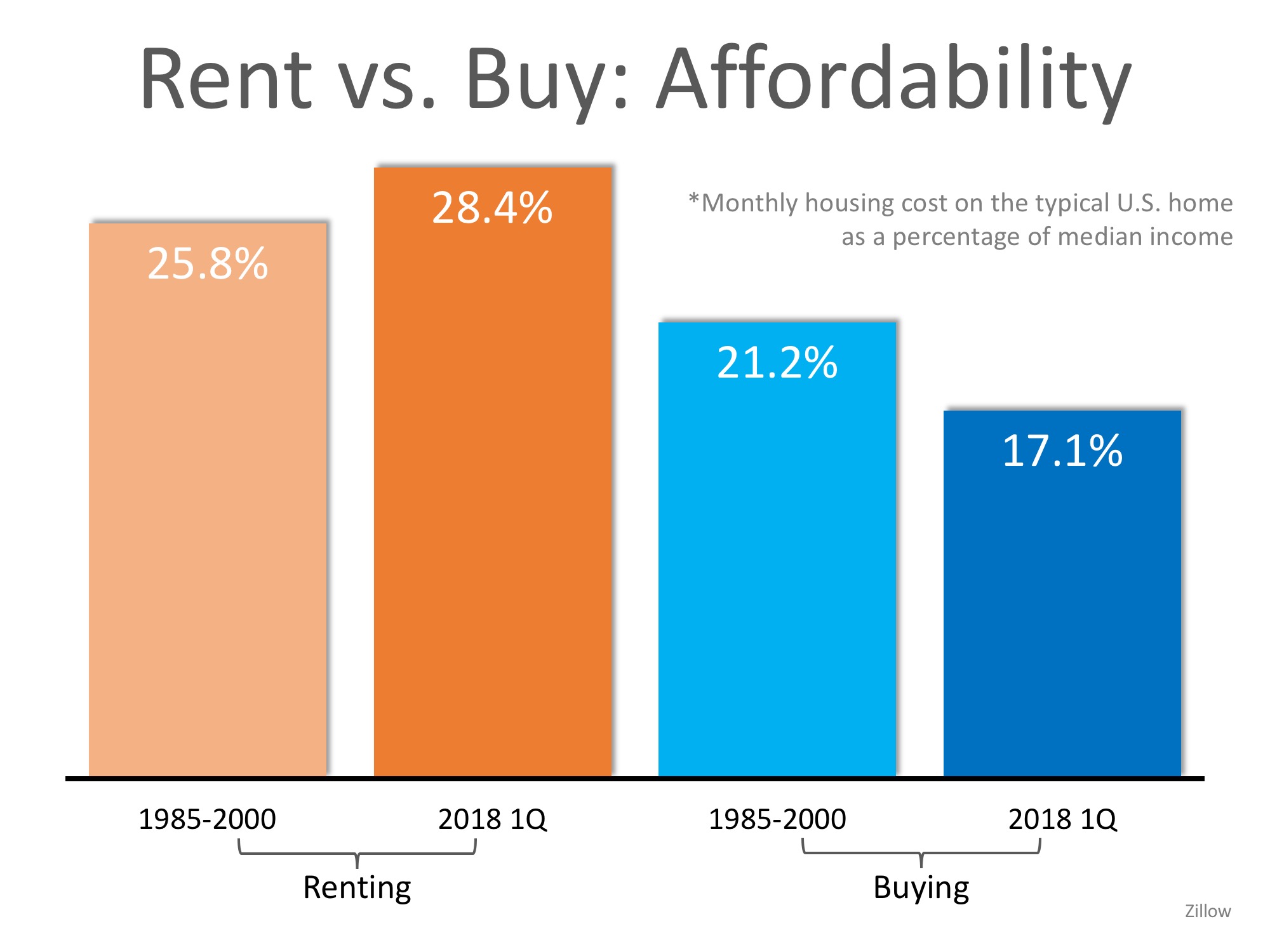

Top 5 Benefits of a VA Home Loan

- The greatest benefit of a VA Loan is that borrowers can buy a home with a 0% down payment.In 2016, 82% of all VA Loans put down 0%!

- Private Mortgage Insurance (PMI) is not required! (Most other loans with down payments under 20% require PMI, which adds additional costs to your monthly housing expense!)

- Credit Score requirements are also lower for VA Home Loans. The average FICO®score of a borrower for an approved VA Loan is 620, compared to 676 (FHA) or 753 (Conventional).

- There is also a limitation on a veteran buyer’s closing costs.Sellers can pay all of a buyer’s loan-related closing costs and up to 4% in concessions in some cases.

- Even with interest rates rising, VA Loans continue to have the lowest average interest rates of all loan types.

Who Qualifies for a VA Home Loan?

One of the most important first steps when applying for a VA Home Loan is obtaining your Certificate of Eligibility (COE). “The COE verifies to the lender that you are eligible for a VA-backed loan.”

You Can Apply for a VA Loan if You:

- Serve 90 consecutive days during wartime

- Serve 181 consecutive days during peacetime

- Have more than 6 years in the National Guard or Reserves

- Are the spouse of a service member who has died in the line of duty or as the result of a service-related disability

You Can Use a VA Loan To:

- Purchase a Home

- Purchase a Condo

- Build a Home

- Refinance an existing home loan

- Make improvements to a home by installing energy-related features or making energy-efficient improvements

Bottom Line

For more information or to find out if you or a loved one would qualify to use the VA Home Loan Benefit, let’s get together! Thank you for your service!

For a Hassle-Free consultation with United Family Mortgage on: Home Refinancing, First-Time Home Buyer Mortgage, Zero-Down Mortgage, Home Construction Loan or VA Home Loan, contact DJ Riley today at 763-276-3960 or via email djriley@unitedfamilymortgage.com.

![]()

*Re-posted by: https://www.mykcm.com/2018/07/04/va-loans-making-a-home-for-the-brave-possible/