There are many clear financial benefits to owning a home: increasing equity, building net worth, growing appreciation, and more. If you’re a renter, it’s never too early to make a plan for how home ownership can propel you toward a stronger future. Here’s a dive into three often-overlooked financial benefits of home ownership and how preparing for them now can steer you in the direction of greater stability, savings, and predictability.

1. You Won’t Always Have a Monthly Housing Payment

According to a recent article by the National Association of Realtors (NAR):

“If you’ve been a lifelong renter, this may sound like a foreign concept, but believe it or not, one day you won’t have a monthly housing payment. Unlike renting, you will eventually pay off your mortgage and your monthly payments will be funding other (possibly more fun) things.”

As a homeowner, someday you can eliminate the monthly payment you make on your house. That’s a huge win and a big factor in how home ownership can drive stability and savings in your life. As soon as you buy a home, your monthly housing costs will begin to work for you as forced savings, coming in the form of equity. As you build equity and grow your net worth, you can continue to reinvest those savings into your future, maybe even by buying that next dream home. The possibilities are truly endless.

As a homeowner, someday you can eliminate the monthly payment you make on your house. That’s a huge win and a big factor in how home ownership can drive stability and savings in your life. As soon as you buy a home, your monthly housing costs will begin to work for you as forced savings, coming in the form of equity. As you build equity and grow your net worth, you can continue to reinvest those savings into your future, maybe even by buying that next dream home. The possibilities are truly endless.

2. Home Ownership Is a Tax Break

One thing people who have never owned a home don’t always think about are the tax advantages of home ownership. The same piece states:

“Both the interest and property tax portion of your mortgage is a tax deduction. As long as the balance of your mortgage is less than the total price of your home, the interest is 100% deductible on your tax return.”

Whether you’re living in your first home or your fifth, it’s a huge financial advantage to have some tax relief tied to the interest you pay each year. It’s one thing you definitely don’t get when you’re renting. Be sure to work with a tax professional to get the best possible benefits on your annual return.

3. Monthly Housing Costs Are Predictable

3. Monthly Housing Costs Are Predictable

A third item noted in the article is how monthly costs become more predictable with home ownership:

“As a homeowner, your monthly costs are most likely based on a fixed-rate mortgage, which allows you to budget your finances over a long period of time, unlike the unpredictability of renting.”

With a mortgage, you can keep your monthly housing costs steady and predictable. Rental prices have been skyrocketing since 2012, and with today’s low mortgage rates, it’s a great time to get more for your money when purchasing a home. If you want to lock-in your monthly payment at a low rate and have a solid understanding of what you’re going to spend in your mortgage payment each month, buying a home may be your best bet.

Bottom Line

If you’re ready to start feeling the benefits of stability, savings, and predictability that come with owning a home, let’s get together to determine if buying a home sooner rather than later is right for you.

For a Hassle-Free consultation with United Family Mortgage on: Home Refinancing, First-Time Home Buyer Mortgage, Zero-Down Mortgage, Home Construction Loan or VA Home Loan, contact DJ Riley today at 763-276-3960 or via email djriley@unitedfamilymortgage.com.

*Re-posted by: https://www.mykcm.com/2020/02/17/the-overlooked-financial-advantages-of-homeownership/

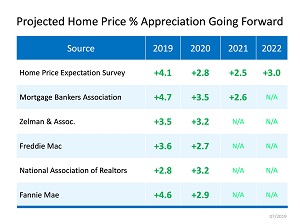

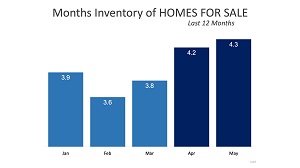

What a difference we’ve seen over the course of this year! If you’re thinking of selling, now is the time as inventory is on the rise.

What a difference we’ve seen over the course of this year! If you’re thinking of selling, now is the time as inventory is on the rise.{kind=link}