With the recent lower interest rates, many homeowners are wondering if they should refinance.

To decide if refinancing is the best option for your family, start by asking yourself these questions:

Why do you want to refinance?

There are many reasons to refinance, but here are three of the most common ones:

- Lower your interest rate and payment– This is the most popular reason. If you have a 5% interest rate or higher, it might be worth seeing if you can take advantage of the current lower interest rates, hovering below 4%, to reduce your monthly payment and overall cost of the loan.

- Shorten the term of your loan– If you have a 30-year loan, it may be advantageous to change it to a 15 or 20-year loan to pay off your mortgage sooner.

- Cash-out refinance– With home prices increasing, you might have enough equity to cash out and invest in something else, like your children’s education, a vacation home, or a new business.

Once you know why you might want to refinance, ask yourself the next question:

How much is it going to cost?

There are fees and closing costs involved in refinancing, and Lenders Network explains:

“If you were to refinance that loan into a new loan, total closing costs will run between 2%-4% of the loan amount.”

They also explain that there are options for no-cost refinance loans, but be on the lookout:

“A no-cost refinance loan is when the lender pays the closing costs for the borrower. However, you should be aware that the lender makes up this money from other aspects of the mortgage. Usually pay charging a slightly higher interest rate so they can make the money back.”

If you’re comfortable with the costs of refinancing, then ask yourself one more question:

Is it worth it?

To answer this one, we’ll use an example. Let’s assume you have a $200,000 home loan. A 4% refinance cost will be $10,000. If you want to lower your interest rate from 6% to 4%, then refinancing is going to save you $244 per month. To break even ($10,000/$244), you need to continue owning your home for over 40 months.

Now that you know how the math shakes out, think about how much longer you’d like to own your current home. If you plan to stay for more than 3 years, then maybe it is advantageous for you to refinance.

If, however, your current home does not fulfill your present needs, you might want to consider using your potential refinance costs for a down payment on a new move-up home. You will still get a lower interest rate than the one you have on your current house, and with the equity you’ve already built, you can finally purchase the home of your dreams.

Bottom Line

There are many opportunities for growth in the current real estate market. To find out what’s right for your family, let’s get together to help you understand your options and guide you toward the best decision.

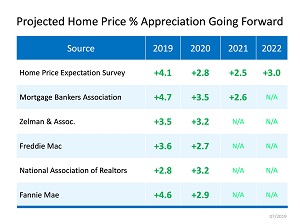

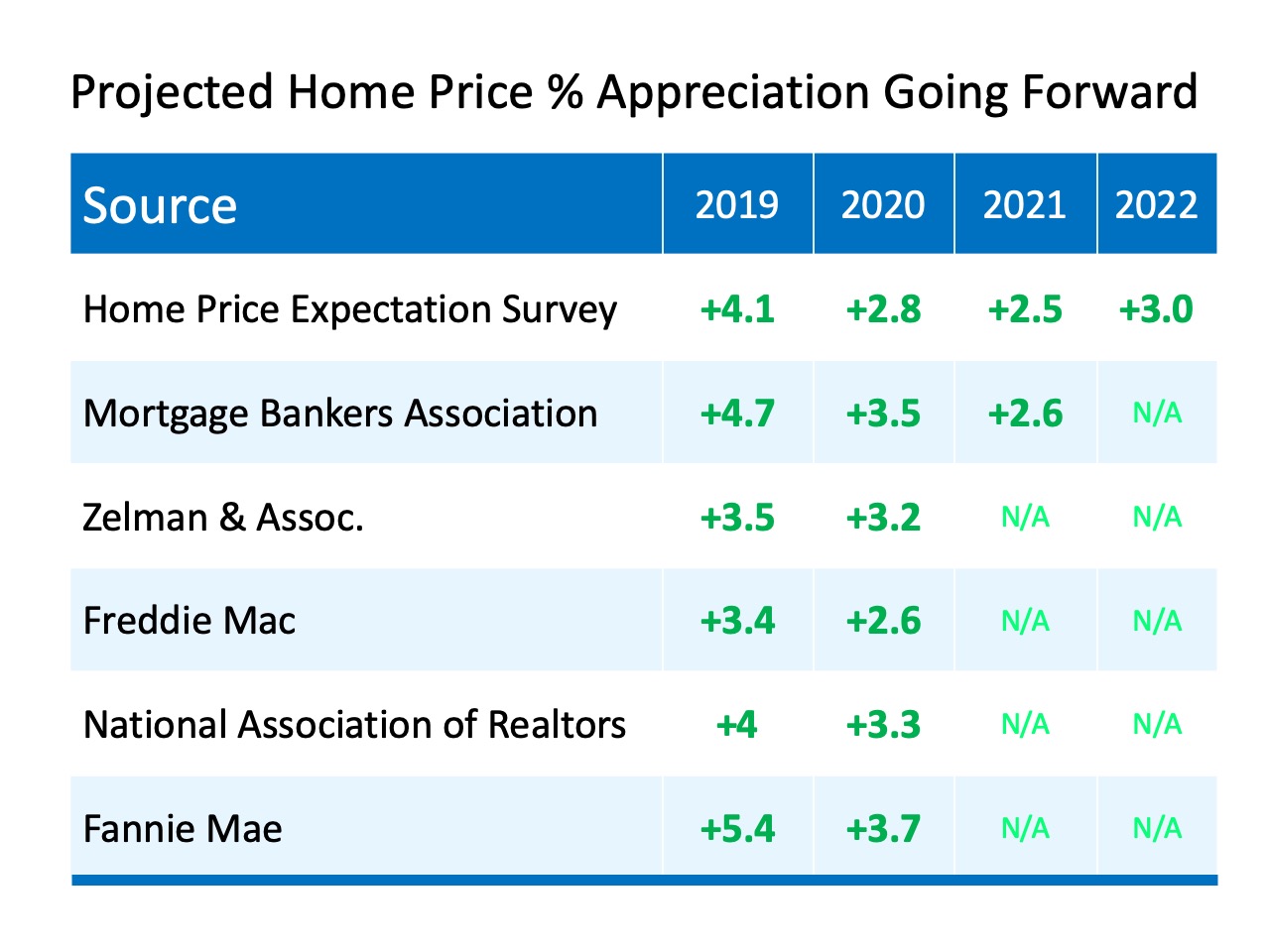

Here’s the home price appreciation these experts are projecting over the next few years:

Bottom Line

Every source sees home prices continuing to appreciate, which is great news for the strength of the market. The increase is steepest throughout the rest of 2019, and prices should continue to rise as we move through 2020 and beyond.

What a Difference a Year Makes for Sellers

Over the last few years, many sellers have been hesitant to put their houses on the market because they feared not being able to find another home to buy.

We’ve reported on inventory shortages in the past, and it’s been a constant concern for potential buyers throughout recent years. New research shows the inventory concern is starting to decrease among potential buyers.

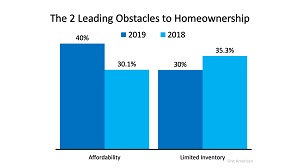

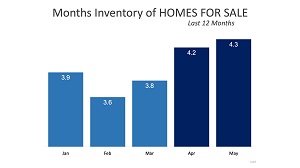

According to First American, the two leading obstacles to homeownership that buyers feel today are Affordability and Limited Inventory. This means the feeling that homes are less affordable has risen, while the fear of limited inventory has decreased, delivering a wealth of good news for sellers.At the same time, over the past 12 months, we’ve seen a steady month-over-month increase in the number of homes coming to market for purchase. In the past, the lack of listings and available inventory slowed down the real estate market. This recent increase in current inventory has many buyers and sellers now thinking it is time to make their move – and rightfully so! For the last two months, we’ve seen over 4 months of inventory become available for sale, a promising number that’s been slowly increasing this year and creating more buying opportunities.To further support the idea of an improving real estate market, Sam Khater, the Chief Economist at Freddie Mac says,

“…In the near-term, we expect the housing market to continue to improve from both a sales and price perspective.”

Many experts, like Sam, believe the second half of 2019 will drive a stronger market than we saw at the beginning of the year. This is great news for homeowners who have put off getting their houses on the market and are now ready to make a move.

Bottom Line

What a difference we’ve seen over the course of this year! If you’re thinking of selling, now is the time as inventory is on the rise.

What a difference we’ve seen over the course of this year! If you’re thinking of selling, now is the time as inventory is on the rise.

For a Hassle-Free consultation on: Home Refinancing, First-Time Home Buyer Mortgage, Zero-Down Mortgage, Home Construction Loan or VA Home Loan, contact DJ Riley today at 763-276-3960 or via email djriley@unitedfamilymortgage.com.

*Re-posted by Keeping Current Matters at: https://www.mykcm.com/2019/07/16/should-i-refinance-my-home/;The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

For a Hassle-Free consultation with United Family Mortgage on: Home Refinancing, First-Time Home Buyer Mortgage, Zero-Down Mortgage, Home Construction Loan or VA Home Loan, contact DJ Riley today at 763-276-3960 or via email djriley@unitedfamilymortgage.com.

For a Hassle-Free consultation with United Family Mortgage on: Home Refinancing, First-Time Home Buyer Mortgage, Zero-Down Mortgage, Home Construction Loan or VA Home Loan, contact DJ Riley today at 763-276-3960 or via email djriley@unitedfamilymortgage.com.

{kind=link}